As we start the New Year of 2018, I wanted to share my experience with a local Calgary business that forced me to learn what rights a consumer has when it comes to signing a contract. I will refrain from naming them, as the purpose of this blog post is meant to inform and educate others of what their rights are as a consumer so that they (hopefully) won’t have a similar experience with contractual agreements. I hold immense gratitude towards this business for allowing me to learn everything that I did learn from this experience. Please note that there is a difference between direct sales contracts (think door-to-door; a vendor comes to you) versus other sales contracts (like an auto dealership; you go to the vendor), however, some basic legal requirements are common to both types of contractual agreements. [UPDATE: November 18, 2020] Here’s a link to the rules and regulations within Alberta regarding door-to-door sales contracts: Dealing With Door-To-Door Sales

On March 19, 2016, I attended a business presentation conference with a woman I was dating at the time, who received a personal invitation from the event organizer. We both connected with and followed a lady we met there on Twitter. In August of 2016, this lady posted a tweet promoting a webinar scheduled for August 17, 2016, and I signed up for the webinar on August 15, 2016. After the webinar, participants were invited to schedule a phone call with her business partner for more information and I scheduled a phone call for August 19, 2016, at 6pm.

The business partner was late in placing his call to me on August 19, 2016. He began the conversation with stories about himself being mentored by Bob Proctor and being at the Calgary Grey Hound bus station with very little money. He then went into the high-pressure sales tactics of “this is the last VIP program spot”, “the price will never be this low again”, and “this is the last opportunity to do this with me”. I had signed a contract with him on August 19, 2016, and paid a $500 deposit. After the phone conversation, I emailed him requesting some time to really think this decision over to ensure it was the best decision for my finances.

On August 22, 2016, I sent another email to cancel my program signup. That day, I received a voice message from the president of his company, a lady, who informed me that I would receive a phone call from him either later that night or the next day. No phone call was ever received. I sent a follow-up email on August 28, 2016, to ensure my program signup had been canceled. I received no further contact from anyone at the company.

On March 8, 2017, I received a missed phone call from an Ontario-based law firm indicating their legal services had been retained by the company for a potential lawsuit case being filed against me. They had asked for more information about my side of things. I forwarded them the email to cancel the program as well as the follow-up email that same night. I phoned back the next morning for confirmation that my emails were received, left a voice message, and received no return phone call.

On May 12, 2017, I received a missed phone call from the same law firm. I spoke to a gentleman who set up a time for one of their associates to contact me at 7am my time (9am EST) on May 15, 2017, and “to prepare for the phone call”.

On May 13, 2017, I received an email notice from my credit report tracking company indicating there were alerts on my credit bureau report. Once I checked into them, I discovered that there was a collection item placed on my credit bureau file by a collection agency that the Ontario-based law firm was using and possibly attempting to sue me without having served me any official documents of a lawsuit or statement of claim. According to standard lawsuit procedure, a statement of claim must be served prior to filing a collection item.

On May 15, 2017, there was no phone call received from the Ontario-based law firm, as per the conversation on May 12th.

On May 16, 2017, I phoned the collection agency after speaking to Equifax (who referred me to them) about the collection item on my credit report. I got routed to a man from the Ontario-based law firm who (in my opinion) was arrogant, belligerent and proceeded to badger me with fear-mongering techniques indicating that “they had proof of the contract being unpaid, involving lawyers would cost me money and he could shave off a couple thousand if I settled.” He also said that the reason for collection item was because “the phone call was scheduled for 9am their time on Saturday, May 13th and because I didn’t respond, they put the collection item on my credit file.” Again, conversation from the 12th had set phone call to be on 15th at 9am EST; in addition, there was no phone call received on the 13th – my phone records show no call being received nor did my call missed call history. A bit of info was let slip while this associate was reading the notes – “Waiting on cancel.”

On May 17, 2017, I received yet another missed call from the law firm (no voice message left). After calling back, I spoke to possibly same person as 16th and provided him with my legal counsel’s contact info. He said that “they’ll be serving a Statement of Claim.” Also, I had requested that going forward, they are to never call my number again and to only contact my legal counsel.

On May 18, 2017, I called Equifax again after speaking to my credit alert company (First Report) who told me that disputing the collection item was something that only Equifax could handle as they were the ones who had the ability to mark it as disputed. Equifax attempted to route me again to the collection agency, however, this time I held my ground and told them that they were the ones with the ability to mark it as disputed and to either tell me what I needed to do or what needed to be done to have that happen. I was asked if I owed anything on the item, to which I replied: “No, I do not”. I was then told that they could launch an investigation into the matter. I asked them to please proceed with launching the investigation.

On May 26, 2017, I received another missed call from the law firm with no voice message left. I didn’t return the phone call as I had already indicated all communication was to be handled by my legal counsel.

On May 30, 2017, I received an email notification from Equifax that my credit file had been amended as requested; meaning the collection item was marked as disputed.

On May 31, 2017, I received a missed phone call from a lady from the collection agency (this being their FIRST EVER attempt to contact me regarding the collection item that was placed on my credit bureau file) regarding the “outstanding balance”. I told her I had retained legal counsel, and after providing her the contact info asked her to contact my legal counsel.

On June 1, 2017, I called Equifax again to have an address issue resolved, as apparently my address was somehow changed by the collection agency with collection item being placed on my credit bureau file. I was informed that for $5.25, I could have a Credit Alert notification on my file for 6 years! This would mean that any and all changes to my credit bureau file would trigger a phone call directly to me to validate the change prior to it actually being made.

VERY IMPORTANT!!!: If you don’t have this, GET IT DONE!!! $5.25 is a drop in the bucket as a price to pay for peace of mind that your credit bureau file is safe for 6 years.

[UPDATE] This recommendation was made prior to the Equifax data breach. The choice is yours if you still wish to proceed with this, however, being that they are only 1 of 2 credit bureau report admins, I would still recommend doing it.

On June 29, 2017, I received a missed phone call from the collection agency again. I decided to call them back even though I had already stated that they were to contact my legal counsel. I was told by the gentleman on the phone that there should’ve been some email correspondence sent to me. I mentioned there was no email correspondence sent to me at all. After listening to him read the notes, the collection agency was apparently directed by the company who lodged the claim (the one I signed the contract with) to close the case and remove the collection item from my credit bureau file, all due to an accounting error. After emailing my legal counsel, the company was somehow unaware that the contract wasn’t signed at a conference. The collection agency, Ontario-based law firm, and the business partner I had signed the contract with were all informed that the contract was deemed null and void in accordance to the Fair Trade Act of Alberta by my legal counsel.

On July 24, 2017, I sent an email to the business partner (2 different email addresses) as well as the associate from the Ontario-based law firm, as an official cancellation of the contract. I also requested the initial deposit be refunded within 15 days, as per the Fair Trade Act of Alberta.

On August 2, 2017, I sent an official mailed letter to the business partner that was the same as email sent on July 24. Nothing has been heard from him.

Since I hadn’t heard anything from the business partner about my deposit, I decided to submit a Better Business Bureau complaint on August 24, 2017, in an attempt to resolve the situation. This is the timeline for it and the correspondence I sent to them.

2017-08-24 web BBB Complaint Received by BBB

2017-08-25 LZ BBB Complaint Validated by BBB Operator

2017-08-25 Otto EMAIL Send Acknowledgement to Consumer

2017-08-25 Otto EMAIL Inform Business of Complaint

2017-09-12 OttO BBB No response to first notice to business

2017-09-12 OttO EMAIL Consumer – Have You Heard From the Company

2017-09-12 OttO MAIL Second Notice to Business

2017-09-21 WEB BBB RECEIVE BUSINESS RESPONSE : We are very grateful for all of our clients and partners. As a company, we strive every day to help them succeed and achieve their goals and objectives.

The client(s) entered into a legally binding contract with our company that clearly states that it is a twelve-month purchase agreement which is non-refundable.

As we are waiting for a legal opinion, we have not yet made a determination as to how we will deal with the outstanding portion of the agreement as executed by Chad Pearen.

Thank you

2017-09-21 LZ EMAIL Forward Business Response to Consumer

2017-09-22 WEB BBB RECEIVED CONSUMER REBUTTAL : (The consumer indicated he/she did not accept the response from the business.)

The contract fails to provide consumer rights under the statutes outlined in the Fair Trade Act of Alberta, which states:

“Absolute cancellation right

27 A consumer may, without any reason, cancel a direct sales contract at any time from the date the sales contract is entered into until, subject to the regulations, 10 days after the consumer receives a copy of the written sales contract.”

The contract failed to provide this right in writing as required by the Fair Trade Act of Alberta. With regards to canceling the contract, it states:

“Effect of cancellation of contract

30(1) A cancellation of a direct sales contract in accordance with this Division operates

(a) to cancel the direct sales contract, or

(b) when the direct sales contract is an offer to buy, to withdraw the offer, as if the direct sales contract never existed.

(2) A cancellation of a direct sales contract in accordance with this Division also operates to cancel

(a) any related sale, RSA 2000

Section 31 Chapter F-2 FAIR TRADING ACT

30

(b) any guarantee given in respect of money payable under the

direct sales contract, and

(c) any security given by the consumer or a guarantor in respect

of money payable under the direct sales contract, as if it never existed.”

This means that under the Fair Trade Act of Alberta, a direct sales contract that is legally canceled must be seen as if it never existed and all security (deposit) must be refunded.

In the eyes of contractual law, the direct sales contract signed isn’t legally binding as it fails on numerous requirements within the Fair Trade Act of Alberta. In addition, any written clause within the direct sales contract stating that a security or deposit is non-refundable is superseded by that of the Regulations set forth in the Fair Trade Act of Alberta, as a consumer cannot under any circumstances, waive their rights under the Fair Trade Act of Alberta.

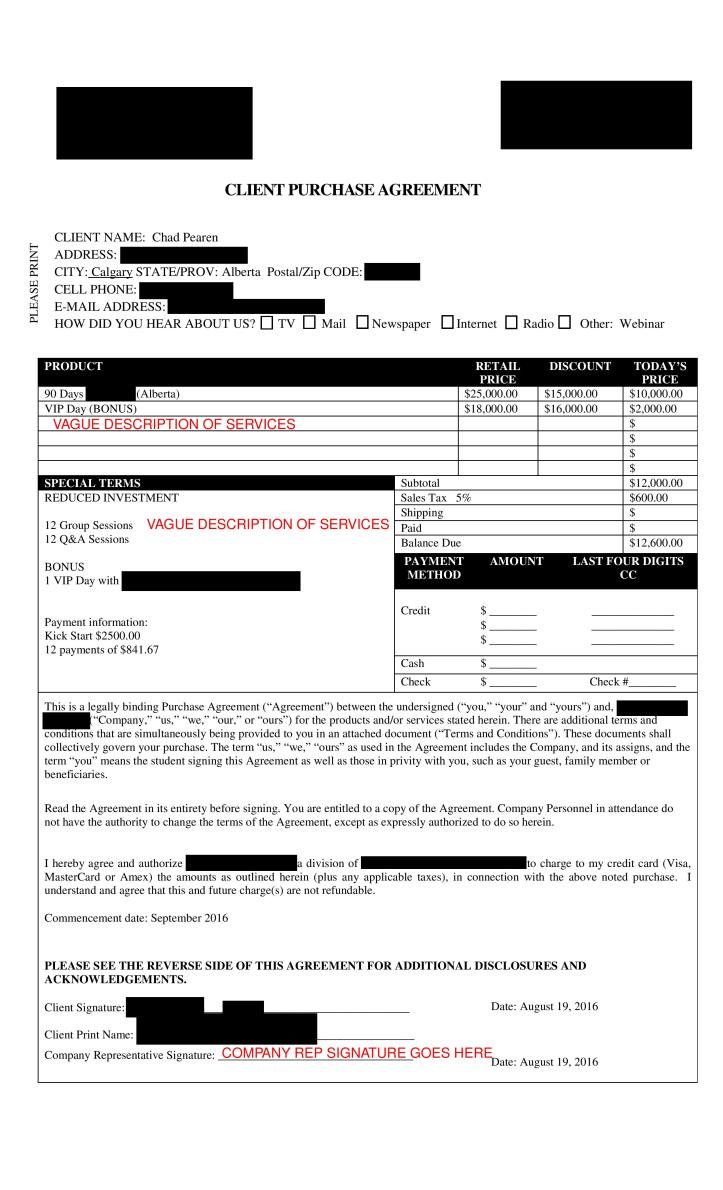

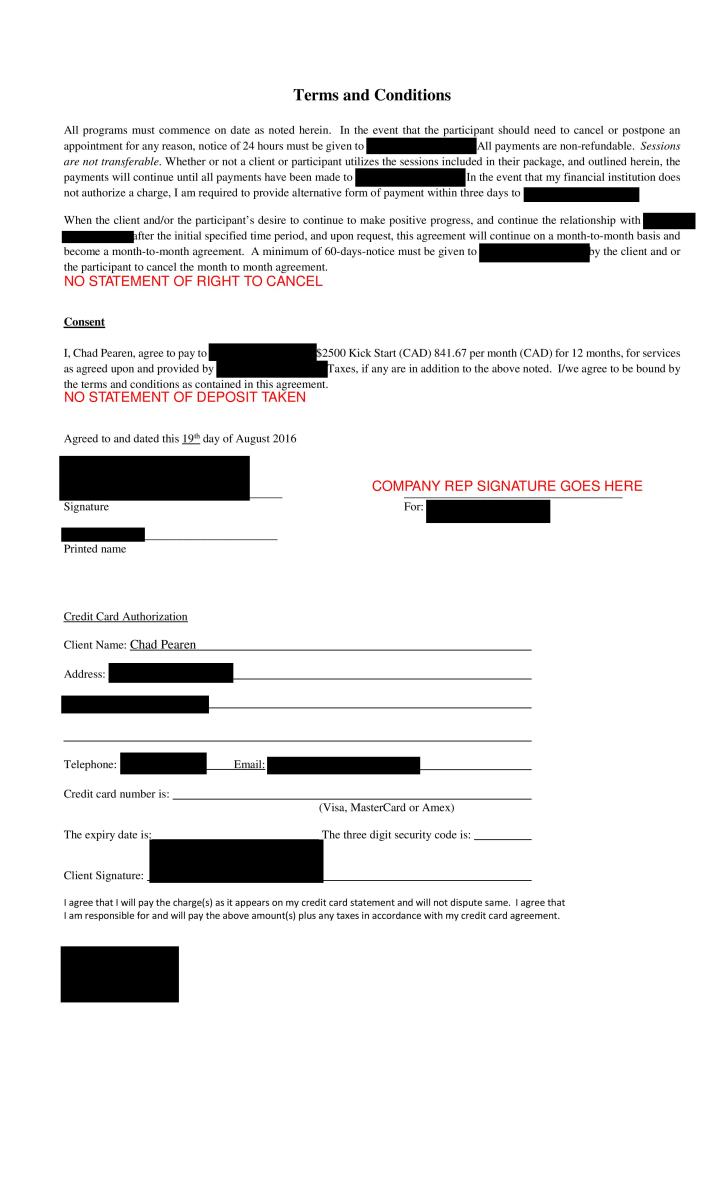

Here’s the only copy of the signed contract in existence, with sensitive/identifying information redacted:

As per the Fair Trade Act, a direct sales contract must include the following:

Contents of sales contract

35 A written direct sales contract must include

(a) the consumer’s name and address;

(b) the supplier’s name, business address, telephone number and, where applicable, fax number;

(c) where applicable, the salesperson’s name;

++++The signed direct sales contract failed to include the salesperson’s name++++

(d) the date and place at which the direct sales contract is entered into;

(e) a description of the goods or services, sufficient to identify them;

++++The signed direct sales contract failed to clearly describe the service(s) provided sufficiently to identify them, as the description(s) provided within the signed contract is very ambiguous++++

(f) a statement of cancellation rights that conforms with the requirements set out in the regulations;

++++The signed direct sales contract failed to include a statement of the right to cancel, as required by the Fair Trade Act++++

(g) the itemized price of the goods or services, or both;

(h) the total amount of the direct sales contract;

(i) the terms of payment;

(j) in the case of a sales contract for the future delivery of goods, future provision of services or future delivery of goods together with services, the delivery date for the goods or commencement date for the services, or both;

(k) in the case of a sales contract for the future provision of services or the delivery of goods together with services, the completion date for providing the services or the goods together with services;

(l) where credit is extended,

(i) a statement of any security taken for payment, and

++++The signed direct sales contract failed to include a statement of security or deposit that was taken for payment, as required by the Fair Trade Act++++

(ii) the disclosure statement required under Part 9;

(m) where there is a trade-in arrangement, a description of and the value of the trade-in;

(n) the signatures of the consumer and the supplier.

++++THE SIGNED DIRECT SALES CONTRACT FAILED TO INCLUDE THE SIGNATURE OF THE SUPPLIER/COMPANY++++

Regulations

36 The Minister may make regulations

(a) specifying amounts for the purposes of section 24(a.1)(i);

(b) respecting the form and contents of the statement of cancellation rights that must be included in a direct sales contract and the form of the contract;

(c) designating places where notices of cancellation may be sent or delivered for the purposes of section 29.

As per the Fair Trade Act, when a direct sales contract has been canceled, the responsibilities of the supplier are as follows:

Responsibilities on cancellation

31(1) In this section,

(a) “authorized person” means

(i) the supplier,

(ii) the person for the time being entitled to possession of the goods, or

(iii) a person specified in the direct sales contract as a person to whom a notice of cancellation may be given;

(b) “consumer’s premises” means the place specified in the sales contract as the consumer’s address or, if the address shown does not specifically identify that place by a municipal address, land description or other description sufficient to distinguish that place from any other, the place where the consumer actually resided at the time the sales contract was made.

(2) Within 15 days after a direct sales contract is canceled, the supplier must refund to the consumer all money paid by the consumer and return to the consumer’s premises any trade-in or an amount equal to the trade-in allowance.

This means that under the Fair Trade Act of Alberta, the supplier is required to refund all security or deposit money paid within 15 days of the consumer canceling the contract. As of today’s date, September 23, 2017, the company has failed to complete this requirement set forth by the Fair Trade Act of Alberta. Above everything else, the company has also failed to provide a SIGNED copy of the direct sales contract (that includes their signature) to me as the consumer.

That’s quite a lot of legal info!!! If you’ve made it through this all, it’s my hope that you’ve found great value in it. Drop a comment below with your thoughts and please share it with others so that more consumers know what their rights are and how to better protect themselves.

🤘